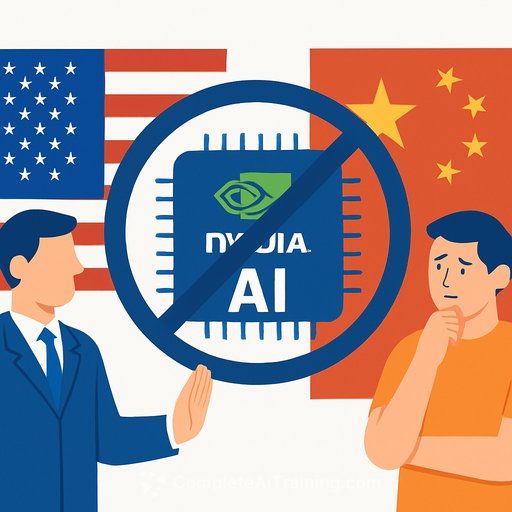

Nvidia's China Freeze: What It Means for Your AI Sales Strategy

Nvidia CEO Jensen Huang says AI chip sales to China are blocked for now. The company is not pursuing approvals to ship its Blackwell line into China, and there are "no active discussions."

Washington's export rules and Beijing's purchasing guidance have effectively shut the door. While H20 chips are allowed by the US, Chinese firms have been told to favor domestic options like Huawei and Cambricon.

What happened

Huang confirmed in Taiwan that Nvidia isn't trying to revive Blackwell shipments to China: "There are no active discussions. Currently, we're not planning to ship anything to China." He added that it's "up to China" to change its policy before Nvidia can serve that market again.

Earlier, the US administration floated raising the Blackwell issue with China's leadership, then stepped back. Meanwhile, Nvidia continues meetings with TSMC and partners globally, while rivals AMD and Broadcom push their own AI chip agendas.

Why sales teams should care

- Supply may tilt outside China: If Blackwell stays out of China, more top-end GPUs could flow to North America, Europe, and parts of Asia. Watch for shorter lead times and new allocation windows.

- China demand is shifting local: Huawei and Cambricon will likely gain share inside China. Global accounts with China operations may split their roadmaps by region.

- Competitive heat rises: AMD and Broadcom will press any opening on price, availability, and interoperability. Expect sharper buyer comparisons and multi-vendor pilots.

- ROI scrutiny tightens: With headlines about export controls and market resets, CFOs will push harder on clear outcomes from AI spend-latency, throughput, time-to-value, and cost-per-inference.

Signals to monitor (and how to respond)

- Beijing policy updates on foreign chips → Prep rapid outreach for waitlisted prospects; share updated ship dates and TCO models.

- US export guidance changes → Refresh compliance checklists and deal desk approvals to avoid surprises late in cycle.

- TSMC capacity notes → Adjust delivery commitments and Q4/Q1 pipeline stages; keep alternatives ready.

- AMD/Broadcom product milestones → Offer bake-offs with clear, customer-owned KPI targets.

- Huawei/Cambricon performance claims in China → For global buyers, propose region-specific stacks with consistent MLOps tooling.

Conversation starters with customers

- "If Blackwell supply loosens outside China, which workloads benefit first-training, fine-tuning, or high-QPS inference?"

- "What's your acceptable queue time and energy cost per token generated? Let's benchmark that on current vs. next-gen hardware."

- "Do you need a dual-vendor plan to hedge supply or pricing? We can structure pilots with identical metrics."

- "How much value do you assign to time-to-deploy vs. absolute peak performance? That trade-off often decides the win."

Action plan for the next quarter

- Re-segment pipeline by urgency and GPU class (H100/H200 vs. Blackwell tiers). Prioritize deals with AI revenue tied to near-term launches.

- Create two pricing paths: performance-optimized and capacity-available. Anchor ROI to customer metrics, not generic benchmarks.

- Bundle services: workload profiling, model compression, and inference optimization to win when hardware is tight.

- Offer region-aware architectures for global enterprises (same MLOps, different silicon where policy requires).

- Tighten compliance steps: export screening, end-use checks, and documented attach of allowed SKUs for China-facing entities.

Quick facts to use in the field

- Nvidia says there are no active efforts to ship Blackwell to China.

- H20 sales are permitted by the US, but China has urged local buyers to choose domestic chips.

- Huang has warned US controls could accelerate Chinese competitors.

- He previously sized Nvidia's potential China opportunity at roughly US$50 billion if fully opened, with China's AI demand projected to grow about 50% per year.

Risk notes for forecasting

- Upside: If supply shifts away from China, some regions may see faster deliveries and larger deal sizes.

- Downside: Policy whiplash can delay signatures. Bake flexibility into MSA language and SOW timelines.

- Competition: Expect tighter discount asks as AMD/Broadcom lean into availability and open software claims.

Helpful links

- Nvidia Blackwell overview

- U.S. BIS export regulations

- AI upskilling paths by job function (including Sales)

Bottom line: China is off-limits for Nvidia's flagship chips-for now. Treat that as a window to win allocations elsewhere, prove ROI fast, and secure multi-year commitments before the next policy shift.

Your membership also unlocks: