Enterprise Token Costs Drop 67% as Multi-Model AI Becomes Standard

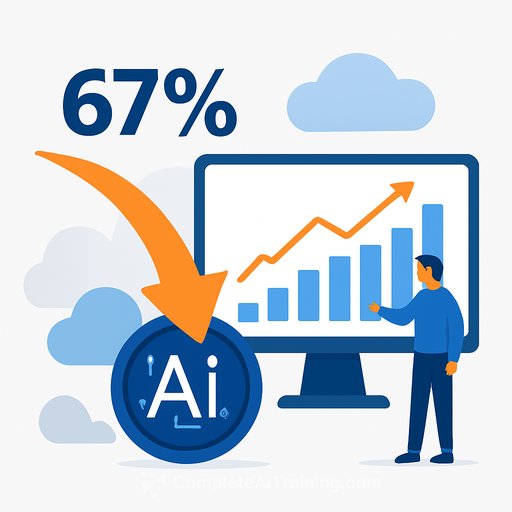

Enterprise teams cut their AI inference costs by two-thirds in the past year by routing work across multiple models instead of defaulting to the most powerful one for every task. That's the headline from AI.cc's 2026 infrastructure report, drawn from 2.4 billion API calls processed across 8,000+ developer and enterprise accounts.

The effective blended cost per million tokens fell from $18.40 to $6.07 between April 2025 and April 2026. For organizations that fully implemented multi-model routing strategies, median costs dropped 87%, according to the report.

Three forces drove the collapse. Open-source models like DeepSeek V4-Flash and Qwen 3.5 established a new price floor. Enterprises stopped over-provisioning expensive frontier models for routine tasks. And AI.cc's aggregation volume secured discounts averaging 23% below direct retail pricing.

The Tiered Intelligence Stack Is Now Default

Multi-model deployment crossed from experimental to standard. Average models per enterprise account reached 4.7 in Q1 2026, up from 2.1 a year earlier.

The dominant architecture now splits work across three tiers. A cost-efficiency tier handles 55-70% of requests using models priced below $0.50 per million input tokens - intent classification, data extraction, batch processing. A mid-performance tier handles 20-30% of requests using models between $0.50 and $5.00 per million tokens - standard response generation, document summarization, customer-facing interactions. A frontier tier handles 5-15% of requests using the most capable models - complex reasoning, long-context analysis, high-stakes decisions where output quality directly affects business outcomes.

The defining characteristic of well-implemented stacks: the frontier tier is reserved strictly for tasks that require it. Teams stopped using Claude Opus or GPT-5.5 as defaults for queries they couldn't confidently classify.

Open-Source Models Now Claim 38% of Enterprise Volume

Open-source and open-weight models captured 38% of enterprise token volume in Q1 2026, up from 11% a year earlier - a 245% share increase.

The top ten models by token volume reflect genuine diversity. Claude Sonnet 4.6 leads by volume. DeepSeek V3.2 ranks second. GPT-5.4 and Gemini 3.1 Flash follow. But Qwen 3.5 9B, Llama 4 Maverick, and GLM-5.1 occupy four of the top ten positions - a mix that would have been impossible a year ago when the list was dominated entirely by OpenAI and Anthropic models.

Open-source adoption is strongest in Europe, where 61% of enterprise token volume flows to open-weight models, driven by data sovereignty and GDPR compliance requirements.

Agent Workflows Are Fastest-Growing Workload

Agent-pattern API calls - sequences of requests with multi-turn reasoning, tool invocation, and iterative refinement - grew 680% year-over-year. These workflows now represent 41% of new integrations, up from 18% a year earlier.

Five dominant agent architectures emerged in production. Research and synthesis agents orchestrate frontier reasoning models for source evaluation alongside fast models for parallel document retrieval. Software development agents chain frontier coding models with mid-tier code review and specialized embedding models for codebase search. Customer experience agents route interactions through classification, standard response, and escalation models. Document processing agents combine vision models for ingestion with reasoning models for extraction. Content production agents coordinate research, generation, quality evaluation, and localization models.

Across all architectures, organizations using AI.cc's OpenClaw agent framework reported lower rates of production incidents from model failures, rate limits, and context management compared to custom-built implementations.

Asia-Pacific Leads Global Adoption

AI.cc's customer base spans 47 countries, with Asia-Pacific representing 44% of active accounts. Singapore, India, Australia, Japan, South Korea, and Indonesia lead the region.

Europe was the fastest-growing region in Q1 2026, with new account activations up 290% year-over-year. North America grew 180%. Middle East and Africa grew 340% from a smaller base. Latin America grew 220%.

Chinese-origin models dominate Asia-Pacific, representing 52% of token volume in the region. European enterprises showed the strongest preference for open-source models. North American teams deployed the highest model diversity at 5.9 distinct models per account.

For product teams building AI-powered features, the data points to a clear direction: multi-model architectures optimized for task-specific routing are no longer experimental. They're the cost baseline. Teams that haven't moved beyond single-model deployments are now operating at a structural cost disadvantage. Understanding which models excel at which tasks - and building routing logic to match them - has become a core product engineering skill.

Your membership also unlocks: